Labuan Malaysia Country-by-Country Reporting Guidelines

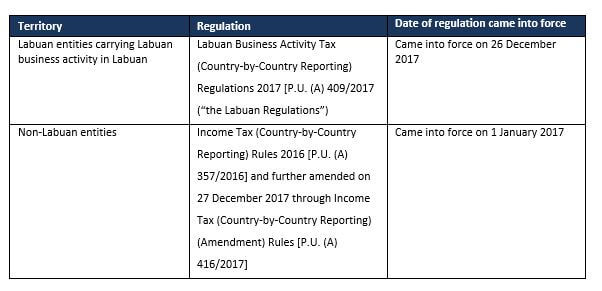

On 26 December 2017, Malaysia Inland Revenue Board (“IRB”) gazetted the Country-by-Country reporting (“CbCR”) regulations for Labuan

entities. The implementation of CbCR will take effect for the financial year starting on and after 1 January 2017. On 1 January 2019, IRB

published CbCR Guidelines for Labuan entities.

In Malaysia, CbCR is governed by two separate regulations as follows:

Labuan is a Federal Territory of Malaysia that maintains its own independent corporate laws and taxation regime from the rest of Malaysia.

How can we help?

Labuan Malaysia Country-by-Country Reporting Guidelines 2019 require careful attention and compliance from multinational enterprises (MNEs)

operating in Labuan. We offer comprehensive services to ensure that your CbCR obligations are met efficiently and accurately. With our

support, you can navigate the complexities of CbCR in Labuan confidently, ensuring compliance and minimising risks associated with

non-compliance.

Our services include:

CbCR in Labuan

With our support, you can navigate the complexities of CbCR in Labuan confidently, ensuring compliance and minimizing risks associated with

non-compliance.

2025 IRAS Indicative Margins for Related Party Loan

Since 2017, the Inland Revenue Authority of Singapore (IRAS) has provided indicative margins to help businesses determine an arm’s length

interest rate for related party loans. In this article we example the margins.

New Singapore Approach to Pricing Intragroup Financing

As of January 1, 2025, new amendments to Singapore's Transfer Pricing (TP) regulations will impact how intra-group loans are

handled—specifically for domestic financing arrangements. These updates introduce significant changes that businesses must consider to

ensure compliance and avoid potential tax penalties. Here’s what you need to know.